Blockchain in Business: Demystifying the Technology and Exploring Practical Applications

Blockchain technology has been making waves in the business world, but many still view it as a complex and enigmatic concept. As a business professional, I have spent considerable time understanding and applying blockchain in various contexts. This article aims to demystify blockchain, providing a clear overview of its core principles and exploring its practical applications in business.

Understanding Blockchain: The Basics

Blockchain is often described as a decentralized ledger, but what does that really mean? At its core, blockchain is a digital ledger of transactions that is duplicated and distributed across the entire network of computer systems on the blockchain. Each block in the chain contains a number of transactions, and every time a new transaction occurs on the blockchain, a record of that transaction is added to every participant’s ledger.

Key Features of Blockchain

- Decentralization: Unlike traditional databases, blockchain does not have a central authority. Instead, it operates on a peer-to-peer network where all participants have equal rights.

- Immutability: Once a transaction is recorded on the blockchain, it cannot be altered or deleted. This ensures the integrity and reliability of the data.

- Transparency: All transactions on the blockchain are visible to all participants, fostering trust and accountability.

Blockchain in Business: Real-World Applications

Blockchain technology is not just a buzzword; it has practical applications that can revolutionize various industries. Let’s explore some of the most prominent use cases.

Supply Chain Management

One of the most significant applications of blockchain in business is in supply chain management. By using blockchain, companies can track the movement of goods from origin to destination in real-time. This transparency helps in identifying inefficiencies, reducing fraud, and ensuring compliance with regulations.

“Blockchain has the potential to transform supply chain management by providing a transparent and immutable record of every transaction.” – [Source Name]

Financial Services

The financial services sector has been one of the earliest adopters of blockchain technology. Blockchain can streamline processes such as cross-border payments, trade finance, and identity verification. By eliminating intermediaries, blockchain can reduce transaction costs and increase processing speeds.

Healthcare

In the healthcare industry, blockchain can be used to securely store and share patient records. This ensures that patient data is accurate, up-to-date, and accessible only to authorized parties. Additionally, blockchain can facilitate the tracking of pharmaceuticals, ensuring that drugs are genuine and have not been tampered with.

Blockchain vs. Traditional Databases: A Comparison

To better understand the advantages of blockchain, let’s compare it with traditional databases.

| Feature | Blockchain | Traditional Database |

|---|---|---|

| Central Authority | No | Yes |

| Data Integrity | Immutable | Can be altered |

| Access Control | Transparent to all participants | Controlled by central authority |

| Scalability | Can be challenging | Generally easier to scale |

| Cost | Higher initial setup cost | Lower initial setup cost |

Challenges and Considerations

While blockchain offers numerous benefits, it is not without its challenges. One of the primary concerns is scalability. As the number of transactions increases, the blockchain network can become slower and more expensive to operate. Additionally, the lack of a central authority can make it difficult to resolve disputes.

Overcoming Challenges

- Scalability Solutions: Technologies such as sharding and layer-2 solutions are being developed to address scalability issues.

- Regulatory Compliance: Businesses must ensure that their use of blockchain complies with local and international regulations.

- Interoperability: Developing standards and protocols to ensure that different blockchain networks can communicate with each other is crucial for widespread adoption.

The Future of Blockchain in Business

As blockchain technology continues to evolve, its applications in business are expected to expand. From smart contracts to decentralized finance (DeFi), the possibilities are vast. However, businesses must approach blockchain with a clear understanding of its capabilities and limitations.

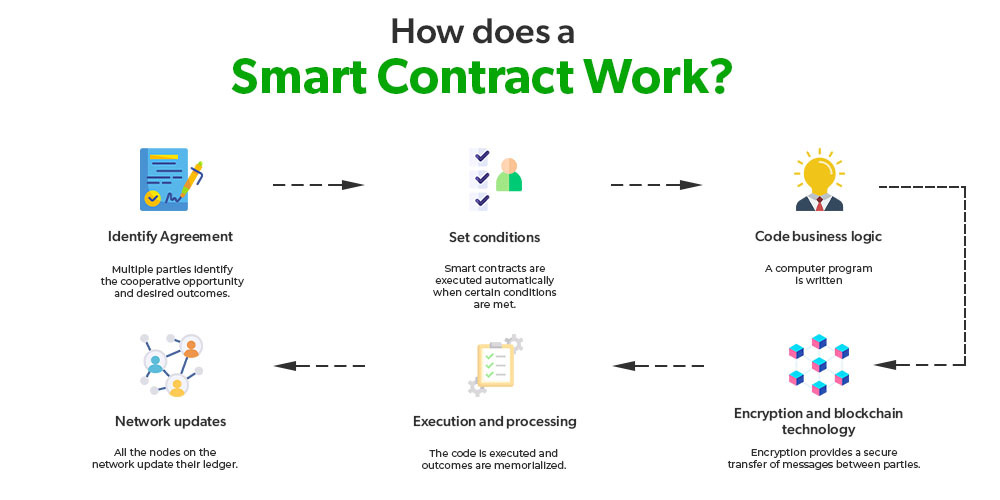

Blockchain and Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automatically execute and enforce the terms of a contract when predefined conditions are met. This can significantly reduce the need for intermediaries and streamline business processes.

Benefits of Smart Contracts

- Automation: Smart contracts automate the execution of agreements, reducing the need for manual intervention.

- Security: Since smart contracts are stored on the blockchain, they are immutable and secure from tampering.

- Cost Efficiency: By eliminating intermediaries, smart contracts can reduce transaction costs and processing times.

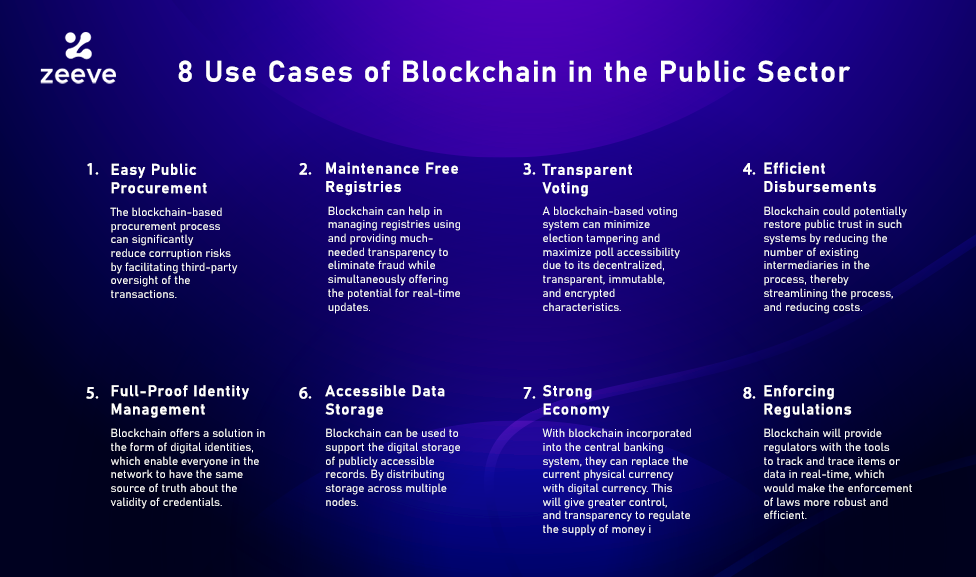

Blockchain in the Public Sector

The public sector is also exploring the potential of blockchain technology. Governments can use blockchain for tasks such as voting systems, land registry, and social welfare distribution. By leveraging blockchain, governments can enhance transparency, reduce corruption, and improve service delivery.

Blockchain and Data Privacy

One of the concerns with blockchain is data privacy. Since all transactions are visible to all participants, sensitive information can be exposed. However, technologies such as zero-knowledge proofs and confidential transactions are being developed to address this issue.

Ensuring Data Privacy

- Zero-Knowledge Proofs: These allow one party to prove to another that they know a value without revealing the value itself.

- Confidential Transactions: These ensure that the amounts transferred in transactions are hidden from public view.

The Role of Blockchain in Digital Identity

Digital identity is another area where blockchain can make a significant impact. By using blockchain, individuals can have control over their personal data, choosing what information to share and with whom. This can enhance privacy and security in the digital age.

Advantages of Blockchain for Digital Identity

- Control: Individuals have control over their personal data, reducing the risk of identity theft.

- Security: Blockchain’s immutability ensures that identity records cannot be altered or deleted.

- Interoperability: Blockchain can facilitate the sharing of identity data across different platforms and services.

Blockchain and Sustainability

Sustainability is becoming increasingly important for businesses, and blockchain can play a role in promoting sustainable practices. For example, blockchain can be used to track the carbon footprint of products, ensuring that they meet environmental standards.

Blockchain for Sustainability

- Carbon Footprint Tracking: Blockchain can provide a transparent and immutable record of a product’s carbon footprint.

- Supply Chain Transparency: By tracking the origin of materials, blockchain can help ensure that products are sourced sustainably.

- Recycling Programs: Blockchain can be used to track the recycling process, ensuring that materials are properly recycled and reused.

The Importance of Education and Training

As blockchain technology becomes more prevalent, it is crucial for businesses to invest in education and training. Employees need to understand the basics of blockchain and how it can be applied in their specific roles.

Training Programs

- Workshops and Seminars: Organizing workshops and seminars can help employees gain a better understanding of blockchain.

- Online Courses: Offering online courses can provide employees with the flexibility to learn at their own pace.

- Certification Programs: Encouraging employees to obtain certifications in blockchain can enhance their skills and knowledge.

The Role of Blockchain in Cybersecurity

Cybersecurity is a growing concern for businesses, and blockchain can offer solutions to enhance security. By leveraging blockchain’s immutability and transparency, businesses can protect their data from cyber threats.

Blockchain for Cybersecurity

- Data Integrity: Blockchain’s immutability ensures that data cannot be altered or deleted, reducing the risk of data breaches.

- Access Control: Blockchain’s transparent nature allows businesses to monitor and control access to sensitive data.

- Secure Transactions: By eliminating intermediaries, blockchain can reduce the risk of fraud and enhance the security of transactions.

Blockchain technology has the potential to transform various aspects of business, from supply chain management to digital identity. However, businesses must approach blockchain with a clear understanding of its capabilities and limitations. By investing in education and training, businesses can harness the power of blockchain to drive innovation and growth.